The latest data released by the American Pet Products Association (APPA) and its 2026 State of the Industry Report provides a clear picture of the US #petmarket’s actual performance in 2025 and its outlook for 2026.

Despite macroeconomic pressure, the industry continues to demonstrate strong resilience. #Petownership penetration is rising, while generational shifts and changing consumption behavior are reshaping the market.

At its core, the industry is moving toward:

- Essential-driven consumption

- More rational spending patterns

Market Size Continues to Expand

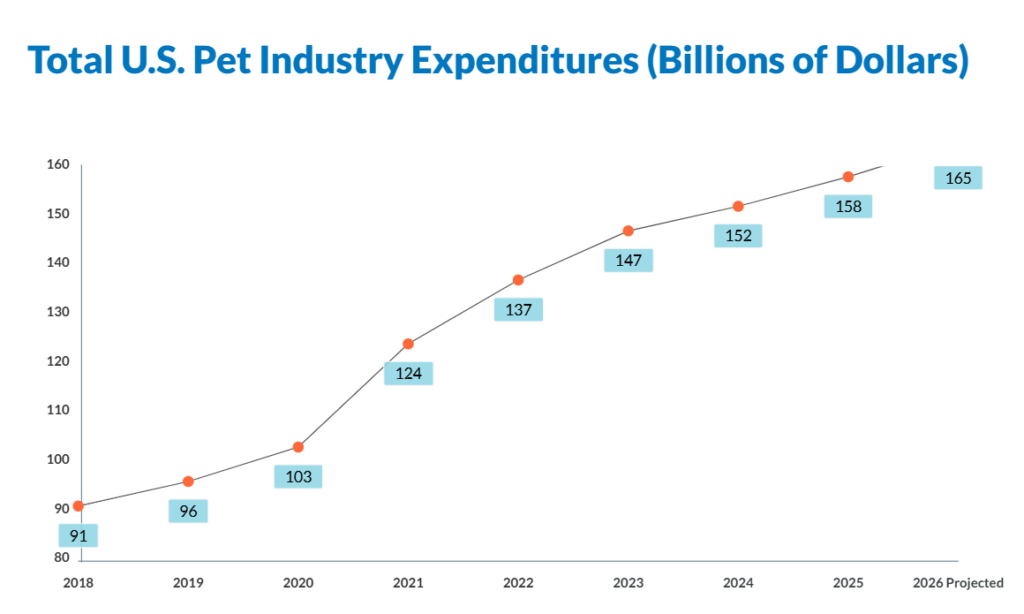

The US #petindustry has maintained a consistent long-term growth trajectory, with total spending increasing year after year.

Key figures:

- 2024 total market size: $151.9 billion

- 2025 total spending: $158.0 billion, up 3.7% YoY (above the earlier forecast of $157.0 billion)

- 2026 projected size: over $165.0 billion, with an estimated growth rate of ~4.4%, including around 2 percentage points driven by inflation

Looking at the longer trend:

- 2018: $90.5 billion

- 2025: $158.0 billion

👉 The market has nearly doubled in 7 years, highlighting a key reality:

Pet-related spending remains highly resilient, even during economic fluctuations.

Four Core Segments Define the Industry Structure

The US pet market is built around four primary spending categories, covering the full lifecycle of pet ownership.

2025 breakdown:

- #Petfood and treats: $68.3 billion

- Supplies, live animals, and OTC medicine: $34.4 billion

- Veterinary care and product sales: $41.0 billion

- Other services (boarding, grooming, insurance, training, pet sitting, walking, etc.): $14.3 billion

2026 projections:

- Pet food and treats: $69.7 billion

- Supplies, live animals, and OTC medicine: $35.6 billion

- Veterinary care and product sales: $42.4 billion

- Other services: $14.9 billion

👉 Two clear signals emerge:

- Veterinary care is the fastest-growing segment, reflecting a shift toward health-focused spending

- Food and treats remain the largest category, acting as the foundation of the industry

This creates increasing pressure for brands operating in everyday product categories such as collars, harnesses, and accessories to maintain relevance within a health-driven market.

Pet Ownership Reaches Record Levels

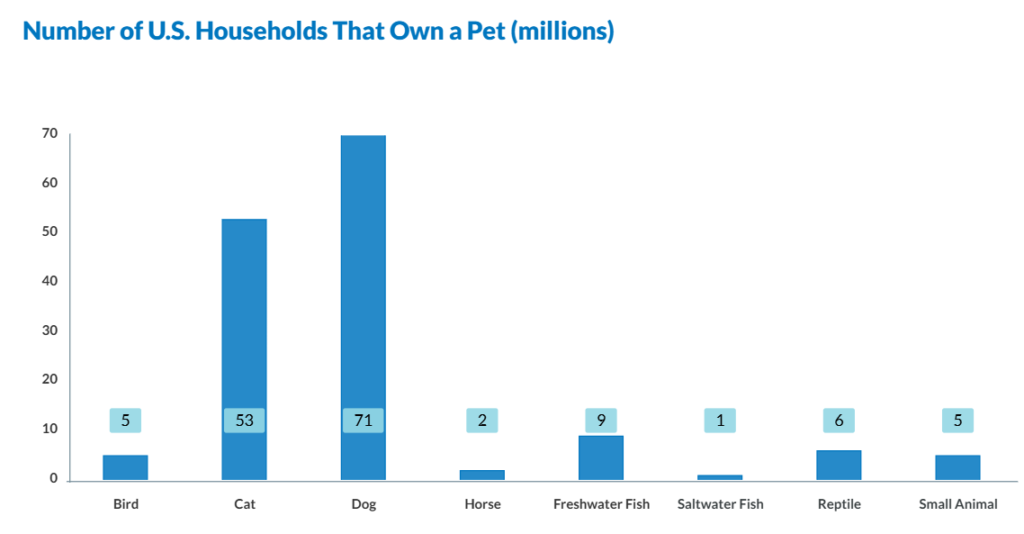

Pet ownership in the US continues to expand.

- 2025 pet-owning households: 95 million, up from 94 million

Breakdown by pet type:

- Dogs: 71 million households (53%), up by ~4 million households

- Cats: 53 million households (39%), growing 5% YoY

- Small pets, birds, reptiles: 6 million households each

- Freshwater fish: 10 million households

- Horses and saltwater fish: 2 million households each

👉 The structure of pet ownership is becoming more diversified, while dogs and cats remain dominant.

Younger Generations Are Driving Market Growth

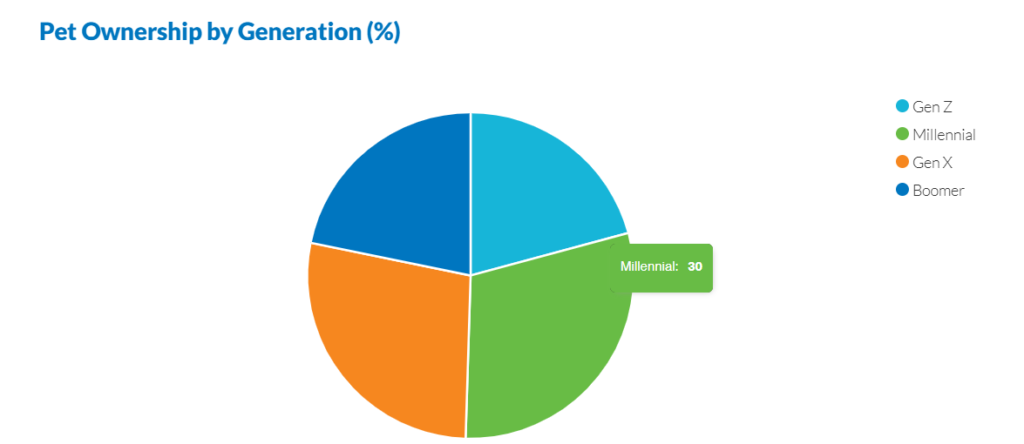

The generational structure of pet ownership has shifted significantly, with younger consumers now leading the market.

Ownership share:

- Millennials: 30% (largest group)

- Gen Z: 20% (fastest-growing)

- Gen X: 25%

- Baby Boomers: 25%

👉 Millennials and Gen Z combined now represent over half of the market.

Behavioral differences:

- Gen Z & Millennials

- Strong emotional connection to pets

- Willing to pay for premium and health-focused products

- Less impacted by economic pressure

- Gen X

- Became a key growth driver in 2025

- Pet ownership increased by 12% YoY

- Growth across multiple categories:

- Dogs: +12%

- Cats: +8%

- Birds: +25%

- Reptiles: +20%

- Freshwater fish: +17%

- Baby Boomers

- More price-sensitive

- Stable but slower growth

👉 This diversification is expanding demand across both mainstream and niche categories.

Consumer Behavior Is Becoming More Rational

Under economic pressure, pet spending behavior is shifting from impulsive to structured decision-making.

Three key patterns:

1. Essential spending remains stable

- Around 50% of #petowners maintain their pet-related spending

- Core categories such as food and veterinary care are prioritized

2. Discretionary spending is being reduced

- 22% of owners are cutting pet expenses (up 10 percentage points YoY)

- Reductions mainly occur in non-essential categories

3. Spending structure is being optimized

- Shift away from premium discretionary items

- Increased focus on:

- Basic care

- Health-related products

👉 This means brands are facing growing pressure to clearly justify product value.

Key Trends Defining 2026

Three major trends are shaping the future of the US pet industry:

1. Continued market expansion

- Growth expected to remain above 4% in 2026

- Driven by both real demand and inflation

2. More diverse consumer base

- Growth is no longer dependent on a single generation

- Driven jointly by:

- Gen Z

- Millennials

- Gen X

👉 Niche #petcategories are gaining new opportunities.

3. Category refinement and polarization

- High-growth areas:

- Veterinary care

- Functional food

- Essential services

- At-risk categories:

- Non-essential products

- Low-differentiation items

👉 Competition is shifting toward:

- Value for money

- Professional and functional positioning

Final Insight

The long-term growth of the US pet industry is fundamentally driven by two forces:

- The humanization of pets

- The essential nature of pet-related spending

As pets become integral members of households, spending around them becomes more resilient and less cyclical.

For brands, the direction is clear:

- Focus on health-driven categories

- Strengthen service differentiation

- Align with the expectations of Millennials and Gen Z

✅ 2️⃣ What This Means for the Pet Industry

The US pet industry is entering a phase defined by:

- Structural growth

- Rational consumption

- Health-driven demand

Key implications:

- Veterinary care and health-related products will continue to lead growth

- Essential categories will remain stable, even under economic pressure

- Non-essential and undifferentiated products will face increasing competition

At the same time:

- Market expansion is becoming more dependent on demographic diversity

- Consumer expectations are shifting toward value, function, and transparency

✅ 3️⃣ What This Means for #PetBrands Working with OEM Partners

The Problem

Brands are facing:

- Rising competition in core categories

- Increasing demand for functional and health-oriented products

- Pressure to justify pricing in a more rational consumer environment

At the same time:

- Inventory risks are increasing

- Margins are under pressure

The Need

To remain competitive, brands need:

- More flexible product strategies

- Faster response to market demand changes

- Reliable quality for health-positioned products

- Better cost control without sacrificing perceived value

Where OEM Partners Create Value

An experienced OEM partner can support brands by:

- Offering flexible production for both essential and functional products

- Enabling smaller batch runs to reduce inventory risk

- Maintaining consistent quality for health-focused positioning

- Providing stable supply chain support in a volatile market

👉 As the industry shifts toward value-driven consumption, OEM partners become a key lever for balancing cost, flexibility, and product competitiveness.