The UK pet population continued to expand in 2026, adding approximately half a million pets over the past two years.

According to new data from UK Pet Food:

- The UK is now home to 36.5 million pets

- These pets live across approximately 18 million households

- At least 62% of British households own a pet

Compared with 2024:

- Pet population increased from 36 million

- Representing growth of 1.4%

The findings are based on the UK Pet Food Pet Population Survey, which included 8,951 interviews conducted in January 2026.

👉 While growth has moderated compared with the pandemic years, pet ownership remains firmly embedded in British households.

Dogs Continue to Lead the Market

Dogs remain the UK’s most popular companion animal and have been the primary driver of pet ownership growth.

The dog population increased:

- From 12.5 million five years ago

- To 13.5 million in 2024

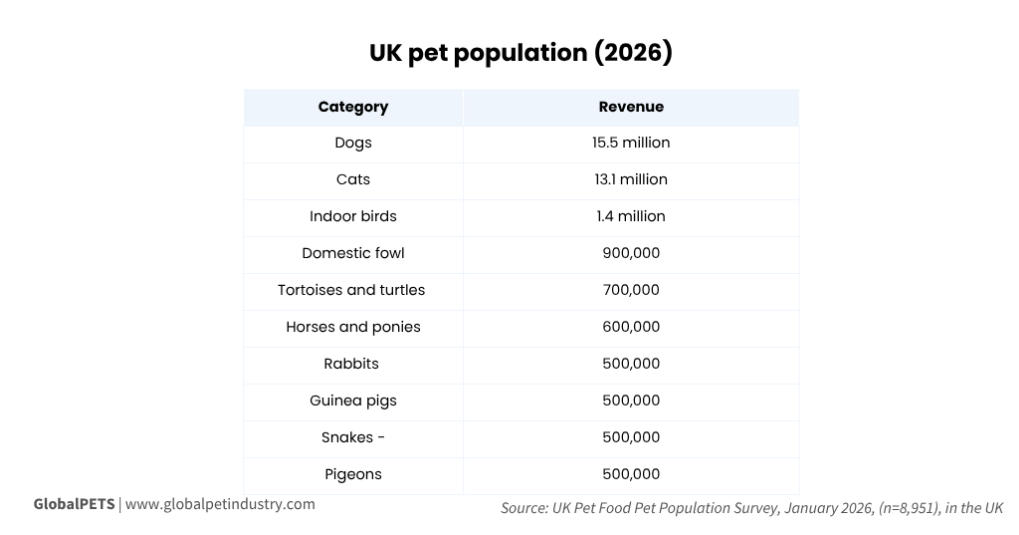

- To 15.5 million in 2026

Household penetration also increased significantly:

- 33% in 2021

- 36% in 2024

- 41% in 2026

👉 This means dog ownership has expanded both in population size and household reach.

For pet brands, this reinforces the long-term importance of dog-focused categories such as:

- Dog food

- Harnesses

- Collars

- Leashes

- Apparel

- Accessories

Cats Maintain Strong Growth Momentum

Cats remain the second most popular #petcategory in the UK.

The cat population reached:

- 13.1 million in 2026

Up from:

- 12.5 million in 2024

Household penetration increased from:

- 29%

- To 31%

👉 Together, dogs and cats account for the overwhelming majority of pet ownership growth in the UK.

Smaller Pet Categories Show Mixed Performance

While dogs and cats expanded, several other pet categories recorded declines.

Indoor Birds

- 1.4 million

- Present in 2.7% of households

Compared with 2024:

- 1.5 million

- 3% household penetration

Domestic Fowl

A more noticeable decline occurred in domestic fowl:

- Approximately 900,000 pets

- Present in 1.1% of households

Compared with:

- 1.3 million

- 1.6% household penetration two years earlier

Tortoises and Turtles

This category remained relatively stable:

- Around 700,000 pets

- Present in 1.6% of households

Consistent with 2024 levels.

Other Niche Pet Categories Remain Stable

Several smaller pet categories maintained similar ownership levels:

- Rabbits:

- Around 500,000

- Present in 1.2% of households

- Guinea pigs:

- Approximately 500,000

- Present in 0.7% of households

- Snakes:

- Around 500,000

- Present in 0.8% of households

- Pigeons:

- Roughly 500,000

- Present in 0.7% of households

Meanwhile:

- Horses and ponies declined from 700,000 in 2024

- To approximately 600,000 in 2026

Household penetration fell from:

- 1.5%

- To roughly 1%

The Long-Term Trend: Pet Ownership Has Rebounded Strongly

One of the most interesting findings is how dramatically pet ownership has evolved over the past decade.

Before the pandemic:

- Household pet ownership declined from 47% in 2011-12

- To 41% in 2019-20

Most pet categories contributed to this decline.

Dogs, however, followed a completely different trajectory.

The dog population increased by:

- 103%

Growing from:

- 7.6 million dogs in 2011

- Across 22% of households

To today’s:

- 15.5 million dogs

- Across 41% of households

Cats also experienced substantial long-term growth.

Their population increased by:

- 68%

Growing from:

- 7.8 million cats

- Across 18% of households

At the beginning of the last decade.

👉 The UK pet market has not simply recovered from previous declines — it has entered a new phase of sustained pet ownership.

Market Revenue Continues to Grow

Pet ownership growth is also translating into higher industry revenue.

According to market data:

- Revenue increased from £4.1 billion ($5.4B / €4.7B) in 2024

- To £4.3 billion ($5.7B / €4.9B) in 2025

Representing:

- 4.9% year-over-year growth

👉 Consumer spending continues to rise even as ownership growth becomes more moderate.

Dog Food Remains the Largest Category

By category share:

Dog Food

- 51.1% of total market sales

Cat Food

- 37.2%

Outdoor Bird Products

- 7.9%

Small Mammals

- 1.5%

Fish

- 1.5%

Indoor Birds

- 0.4%

👉 Food continues to dominate spending across the UK pet market, with dogs remaining the largest revenue driver.

Final Insight

The UK’s pet market continues to demonstrate strong long-term fundamentals.

While overall population growth has become more measured, several trends remain clear:

- Pet ownership remains historically high

- Dogs and cats continue gaining household penetration

- Industry revenue is still increasing

- Consumer spending remains resilient

👉 The UK is no longer experiencing a temporary pet ownership boom.

Instead, it appears to be entering a more mature phase where pets occupy a permanent and increasingly important role within British households.

For brands, the opportunity is shifting from simply attracting more pet owners toward delivering greater value, functionality, and premium experiences to an already engaged consumer base.

✅ 2️⃣ What This Means for the Pet Industry

The UK market reinforces several long-term industry trends:

- Pet ownership remains deeply integrated into household life

- Dogs and cats continue to dominate category growth

- Consumer spending is increasing faster than pet population growth

- Mature markets continue moving toward premiumization and value-added products

At the same time:

👉 Growth is becoming increasingly dependent on spending per pet rather than simply adding new pet owners.

This creates opportunities for brands that can offer:

- Better functionality

- Higher quality

- More specialized products

Source: GlobalPETS