Pet-related costs continued to move upward across major global markets in February, reinforcing ongoing pressure on brands and consumers. At the same time, geopolitical tensions and supply chain disruptions are increasing the likelihood of further inflation in the months ahead.

After January showed signs of stabilizing the fluctuations seen in 2025, February confirmed a consistent upward trend. Across all 5 markets tracked by PETS International, prices for #petfood, #petsupplies, and services increased month-on-month (MoM).

Europe

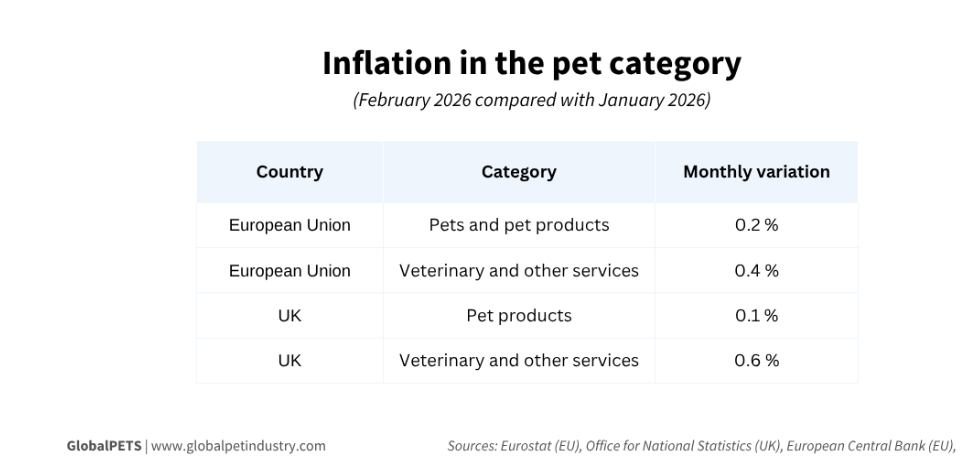

Across the European Union, the Consumer Price Index (CPI) for pet-related products rose by 0.2% in February 2026 compared to January, reflecting steady cost pressure across the region.

According to Eurostat data:

- Estonia (+4.9%) and Latvia (+2.8%) recorded the strongest increases, following sharp declines in January — indicating a normalization effect

- Cyprus (-1.7%) and Finland (-1.4%) experienced the largest price decreases

Meanwhile, veterinary and pet-related services rose faster than products, increasing by 0.4%:

- Slovenia saw a significant surge of 9%, nearly three times higher than Slovakia (3.4%)

- Bulgaria was the only country where prices declined, falling by 0.3%

From a broader economic perspective, both the EU and the Eurozone saw overall CPI rise by 0.6% in February, driven by higher costs in:

- Services

- Food

- Alcohol and tobacco

- Non-energy industrial goods

👉 This widening cost pressure is making it increasingly difficult for #petbrands to maintain stable pricing strategies across multiple European markets.

UK

In the UK, #petproduct prices continued their gradual increase, rising by 0.1% in February, consistent with January’s pace.

However, veterinary and #petservices showed a clear acceleration:

- January: +0.1%

- February: +0.6%

Overall CPI in the UK rose by 0.4%, primarily driven by clothing, while partially offset by lower motor fuel prices.

A notable structural change in the market:

The Office for National Statistics (ONS) officially added #petgrooming to its inflation basket in March.

This reflects:

- The growing importance of grooming services

- Its position as the second-highest spending category after veterinary health checks

Other tracked pet-related categories include:

- Pet food and treats

- #Petcollars and accessories

- Animal cages

- #Petinsurance

- Boarding services

👉 This signals a shift where not only essential products but also service-based categories are becoming key cost drivers in the #petindustry.

US

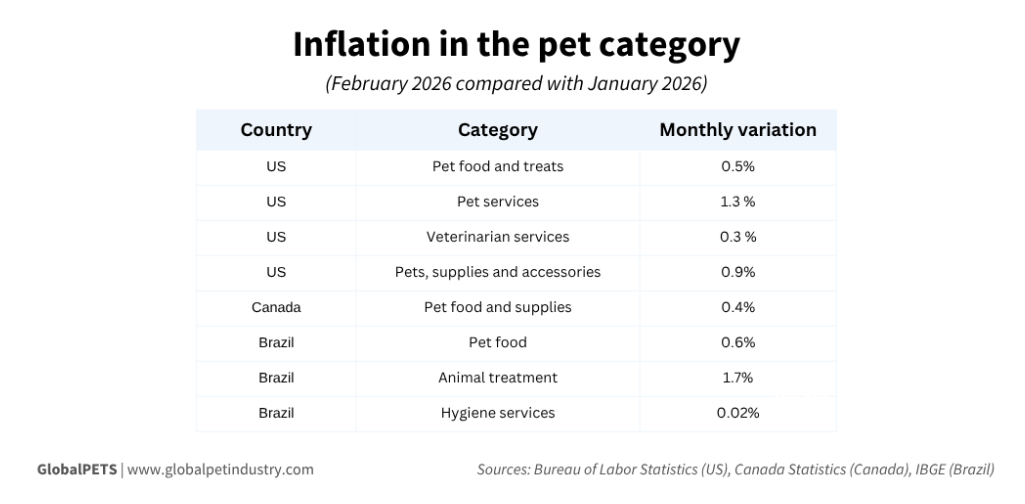

The US market recorded price increases across all monitored #petcategories, with particularly strong momentum in services.

- Pet services: +1.3% (highest increase)

- Supplies and accessories: +0.9% (after a 1% decline in January)

- Pet food and treats: +0.5%

- Veterinary services: +0.3%

The overall CPI rose by 0.3% in February, slightly higher than January’s 0.2%.

Key contributing sectors included:

- Medical care

- Apparel

- Household furnishings

- Airline fares

- Education

👉 Rising service and product costs are forcing brands to reassess pricing structures, especially in everyday categories like harnesses, leashes, and collars where margins are already tight.

Canada

In Canada, pet food and supplies returned to a more stable growth pattern after a sharp increase in January (+2.3%).

- February increase: +0.4%

Overall CPI rose to 0.5%, influenced by the expiration of a temporary tax benefit (December 14, 2024 – February 15, 2025), which resulted in higher consumer prices.

👉 This kind of policy-driven fluctuation creates additional uncertainty for brands trying to plan inventory and pricing strategies.

Brazil

Brazil showed mixed dynamics across different pet categories:

- Veterinary treatment: +1.7% (highest increase)

- Pet food: +0.6%

- Hygiene services: +0.02% (sharp slowdown from 1.1% in January)

The country’s overall inflation reached 0.7%, more than double the previous month, marking the highest increase in a year.

This was largely driven by:

- Adjustments in school tuition fees

👉 Volatility across categories highlights how uneven cost pressure can impact different segments of the #petmarket.

Inflation Outlook

Looking ahead, inflation is expected to continue rising globally.

Key drivers include:

- Ongoing geopolitical tensions in the Middle East (Iran, the US, Israel)

- Supply chain disruptions

- Rising logistics and energy costs

Major institutions such as S&P Global and ING warn that:

- Energy shocks could significantly push inflation higher

- Consumer spending may weaken

- Central banks may delay policy easing

In Europe, reliance on imported LNG is a critical risk factor, with potential disruptions leading to higher energy costs and broader inflationary pressure.

Additional analysis from Jefferies indicates that:

- Packaged food costs will rise further due to increases in freight, packaging, and processing

👉 These combined pressures are pushing brands to look for more cost-controlled, flexible, and resilient supply chain solutions.

✅ 2️⃣ What This Means for the Pet Industry

The global pet industry is entering a phase of sustained and structurally driven inflation.

Key shifts include:

- Cost increases are no longer limited to products — services are now a major inflation driver

- Price volatility varies significantly by region and category

- External factors (energy, logistics, geopolitics) are becoming dominant influences

This creates a more complex operating environment where:

- Pricing strategies are harder to standardize

- Demand sensitivity may increase

- Market segmentation (essential vs non-essential products) becomes more pronounced

✅ 3️⃣ What This Means for Pet Brands Working with OEM Partners

The Problem

Brands are facing:

- Rising production and service costs

- Increasing pricing pressure across markets

- Uncertainty driven by supply chain disruptions and policy changes

Maintaining margins while staying competitive is becoming significantly harder.

The Need

To adapt, brands need:

- Better cost control mechanisms

- More flexible production planning

- Faster response to market changes

- Stable and reliable supply chains

Where OEM Partners Create Value

This is where the right OEM partner becomes critical.

A strong OEM setup can help brands:

- Optimize cost structures through direct manufacturing

- Enable small-batch, flexible production to reduce inventory risk

- Shorten lead times to react faster to price changes

- Ensure supply chain stability despite external disruptions

👉 In a high-inflation environment, OEM is no longer just about production — it becomes a strategic tool for risk management and competitiveness.

Source: GlobalPETS