The latest report from PLMA shows that in 2025, U.S. private label products achieved record highs in both sales and market share, even under economic pressure.

Among all categories, pet care stood out as one of the strongest growth drivers.

👉 This signals a structural shift:

Private label pet products are no longer just a low-cost alternative — they are becoming a core engine of retail growth.

(For the full report, please send a private message.)

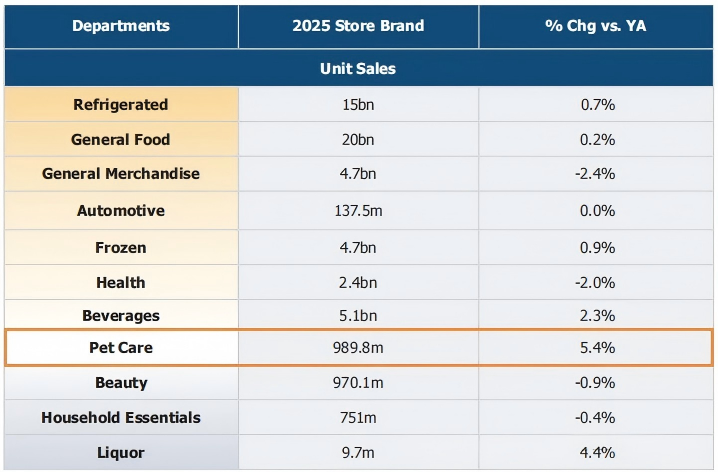

Strong Performance Across the Category

Leading Growth at the Department Level

In 2025, private label pet care outperformed most retail categories:

- Unit sales increased by 5.4% (the highest among all departments)

- Dollar sales grew by 3.7%, ranking fourth among growing categories

By comparison:

- Alcohol: +4.4%

- Beverages: +2.3%

Total performance:

- Sales reached $5.6 billion

- Unit volume reached 989.8 million units

- Market share:

- 17.2% (value)

- 18.1% (unit)

👉 Pet care has become a core pillar within non-food private label categories.

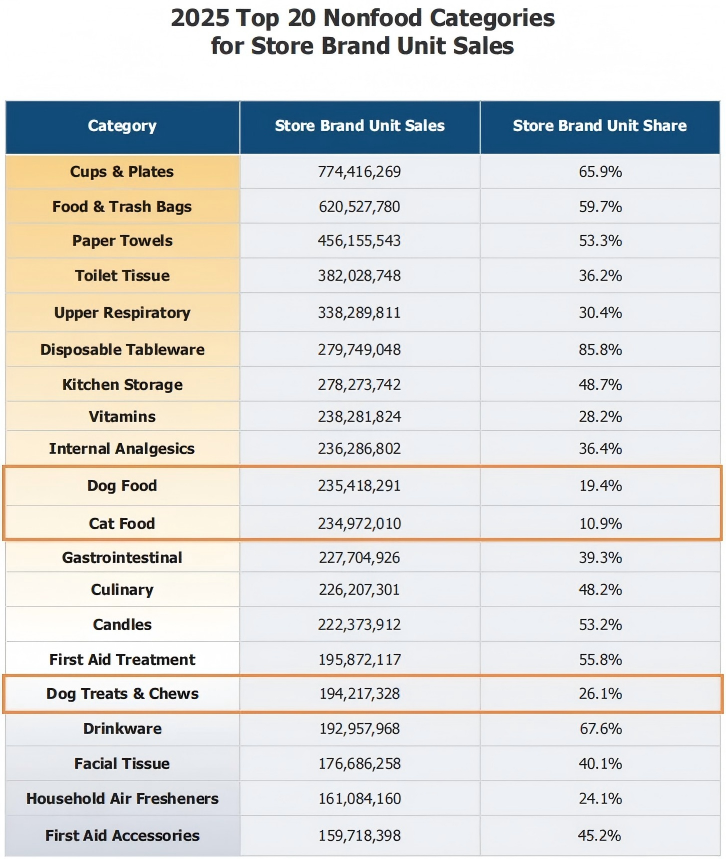

Core Categories Drive Volume — But New Segments Are Expanding Fast

Core Categories

Dog food and dog treats remain the backbone:

- Dog food:

- $1.433 billion in sales

- 13.3% market share (value)

- 235 million units, 19.4% share (unit)

- Dog treats & chews:

- $1.155 billion in sales

- 23.1% share (value)

- 194 million units, 26.1% share (unit)

Meanwhile:

- Cat food reached 235 million units

- Holding 10.9% share, entering the Top 20 non-food categories

👉 This confirms:

Core feeding categories remain stable — but competition is intensifying.

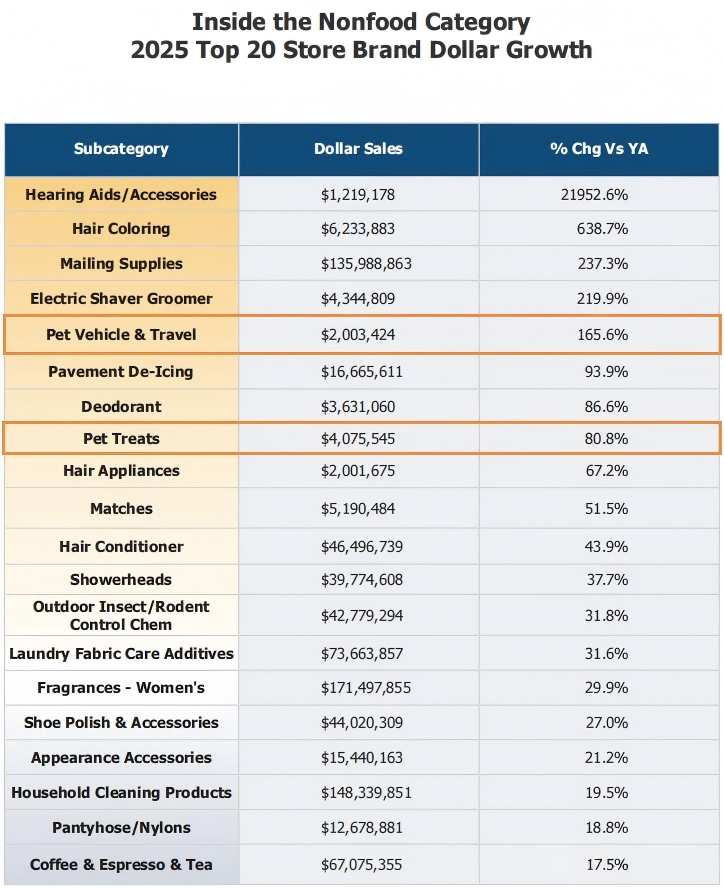

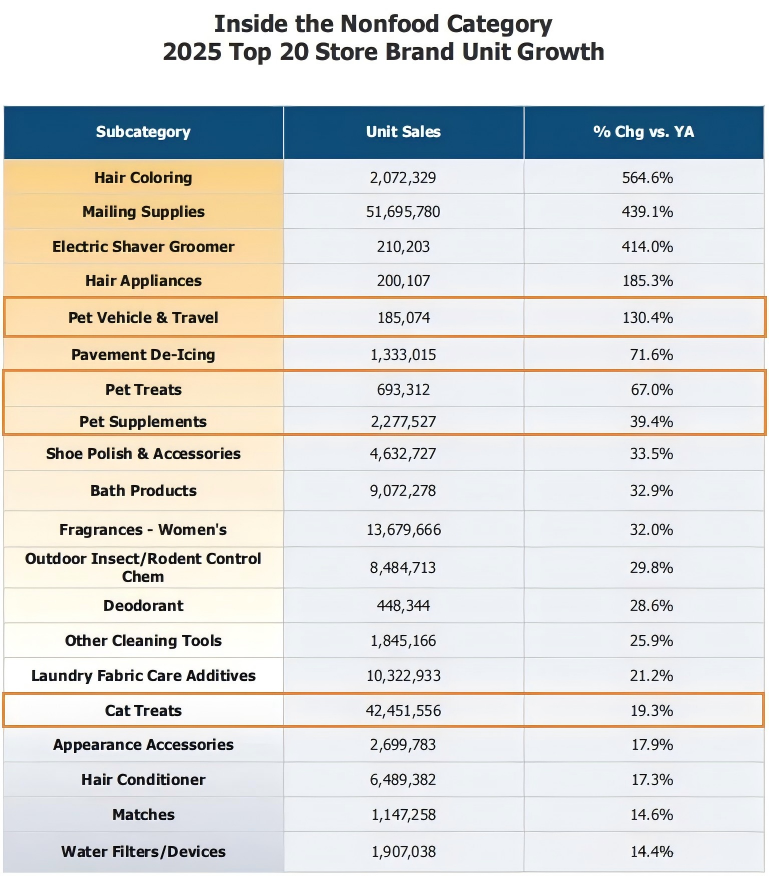

Emerging Subcategories: The Real Growth Drivers

New segments are expanding much faster than traditional categories.

Key highlights:

- Pet travel products:

- +165.6% (value)

- +130.4% (unit)

- Pet treats subcategories:

- +80.8% (value)

- +67% (unit)

Other fast-growing areas:

- Supplements: +39.4% (unit)

- Cat treats: +19.3% (unit)

👉 This reflects a major shift:

Pet consumption is moving from basic feeding → refined care and lifestyle products.

What’s Driving the Growth?

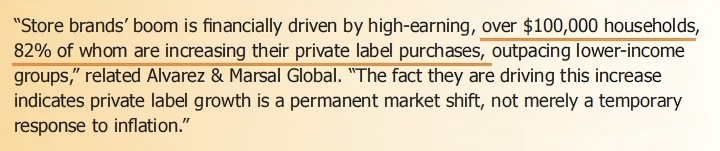

1. Consumer Shift: High-Income Households Are Leading

One of the biggest changes:

👉 Private label growth is no longer driven by low-income consumers.

Instead:

- 82% of households earning over $100K are increasing private label purchases

At the same time:

- Over 80% of consumers believe private label pet food quality is equal to or better than

- 90% recognize its value for money

Retail trust also plays a role:

- 59% of consumers trust private label because of retailer endorsement

- This trust is even higher among Millennials and Gen Z

👉 This changes the competitive landscape:

Private label is no longer about price — it’s about perceived value and trust.

2. Retail Strategy: Private Label as a Differentiation Tool

Major retailers are investing heavily in private-label pet products.

Examples:

- Costco (Kirkland Signature):

- “Same quality, 20% lower price”

- Accounts for roughly one-third of Costco’s revenue

- Walmart (bettergoods):

- Premium positioning

- Focus on plant-based and organic

- Kroger, Target, Amazon:

- Expanding private label lines (Smart Way, Figmint, Saver)

👉 Retailers are no longer just selling products — they are building exclusive product ecosystems.

3. Industry Support: A More Mature Private Label Ecosystem

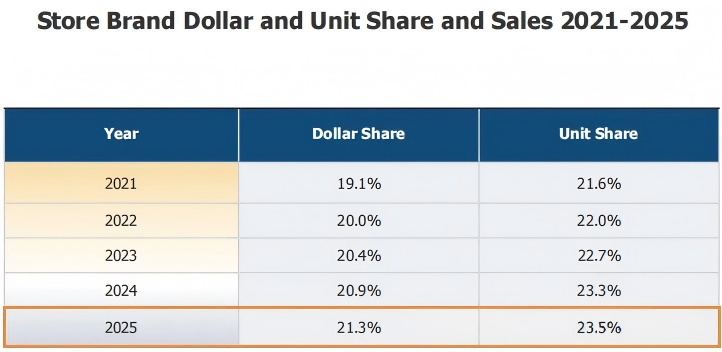

Private label overall reached:

- 21.3% value share

- 23.5% unit share

Innovation trends include:

- Plant-based

- Health-focused

- Sustainable products

These trends are extending into pet categories:

- Grain-free

- Probiotics

- Skin & coat health

At the same time:

- The 2025 PLMA Chicago show hosted 1,900+ exhibitors

- Showcasing 50,000+ products, with a growing pet category presence

👉 The ecosystem is now mature enough to support rapid category expansion.

Future Trends: From Scale Growth to Value Growth

PLMA highlights that private label growth is not temporary —

👉 it represents a permanent structural shift.

Pet private label is moving into a new phase:

1. Segmentation: Expanding Into Niche Needs

Growth will come from:

- Travel products

- Supplements

- Oral care

- Customized grooming

As well as:

- Breed-specific

- Age-specific

- Size-specific products

👉 Brands are being pushed to serve more precise consumer needs.

2. Premiumization: “Affordable Luxury” Becomes Standard

Retailers are building tiered strategies:

- Entry-level

- Mid-tier

- Premium

Since 2021:

- The Premium tier has grown 76%

In pet categories, this translates to:

- Better ingredients (organic, grain-free, human-grade)

- Functional benefits (low-fat, hypoallergenic, digestive support)

- More refined packaging

👉 The goal is clear:

Offer premium quality without premium pricing.

3. Proprietary Products: The Next Competitive Barrier

The next stage of private label evolution:

👉 Exclusive, retailer-owned products

Examples include:

- Unique formulations

- Limited-edition treats

- Customized accessories

Retailers will:

- Deepen collaboration with suppliers

- Build exclusive product portfolios

👉 Differentiation will come from what only you can offer.

4. Marketing: Content and Social Are Becoming Standard

Retailers are increasingly using:

- Influencers

- Social media campaigns

For pet products:

- Pet influencers

- Product reviews

- Lifestyle content

Combined with:

- In-store experiences

👉 Online + offline integration is becoming essential.

5. Supply Chain Integration: A Strategic Priority

Retailers are strengthening partnerships with private label suppliers.

Example:

- Lidl emphasizes close supplier collaboration

This applies directly to pet products:

- Quality control

- Cost management

- Faster product development

👉 Even smaller retailers are investing in supply chain capabilities.

Final Insight

The U.S. private label pet market has moved beyond:

👉 “low-cost alternative.”

It is now defined by:

- Quality

- Innovation

- Brand positioning

👉 Competition is shifting from price → value.

✅ 2️⃣ What This Means for the Pet Industry

The rise of private label is reshaping the pet industry:

- Growth is no longer driven only by brands

- Retailers are becoming product creators

- Competition is moving toward value and differentiation

At the same time:

- Consumer expectations are increasing

- Product segmentation is becoming more detailed

- Innovation is accelerating across categories

👉 The industry is shifting from volume competition → value competition.

✅ 3️⃣ What This Means for Pet Brands Working with OEM Partners

The Problem

Brands and retailers are facing:

- Increasing pressure to differentiate

- Rising expectations on product quality

- Faster product development cycles

- Need for exclusive offerings

The Need

To compete, they require:

- Flexible product development

- Ability to create exclusive SKUs

- Strong cost-performance balance

- Reliable and scalable production

Where OEM Partners Create Value

OEM partners play a critical role by:

- Supporting the development of proprietary products

- Enabling fast iteration of new categories

- Providing cost-effective production solutions

- Ensuring a stable supply for growing demand

👉 In a private label-driven market, supplier capability directly impacts brand competitiveness.

One Response

(For the full report, please DM me.)