Germany’s pet population recorded another slight decline in 2025, continuing a gradual downward trend seen over recent years.

However, despite softer ownership numbers, overall market revenue remained relatively stable — highlighting the resilience of pet-related spending even in a mature market environment.

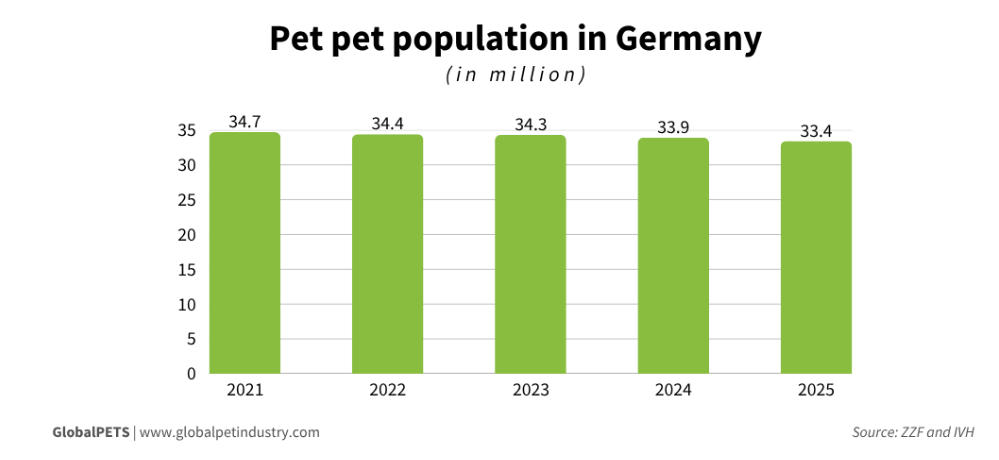

According to data from the German Pet Trade & Industry Association and the Industrial Association of Pet Care Producers:

- Germany had 33.4 million pets in 2025 (excluding fish and reptiles)

- 43% of households owned at least one pet

Compared with previous years:

- 2024: 33.9 million pets, 44% household penetration

- 2023: 34.3 million pets, 45% household penetration

- 2022: 34.4 million pets, 46% household penetration

👉 The decline is gradual rather than dramatic.

But it suggests the German market may be entering a more mature and stable phase.

Ownership Trends: Older Consumers and Families Remain Core Drivers

The 2025 study, based on a survey of 5,000 households, reveals clear differences in ownership patterns.

Household Size

Pet ownership distribution:

- Single-person households: 26%

- Two-person households: 35%

- Households with 3+ people: 39%

Families continue to play an important role:

- 67% of households with children owned at least one pet

In addition:

- 13% of households owned two or more types of pets

Older Consumers Represent a Large Share of Owners

By age group:

- 60+ years old: 25%

- 50–59 years old: 21%

Younger ownership rates were lower:

- 30–39 years old: 19%

- 40–49 years old: 18%

- Under 29: 17%

👉 This highlights an important demographic reality:

Older consumers remain a key purchasing force in Germany’s pet market.

Cats and Dogs Still Dominate — Despite Slight Declines

Cats remain Germany’s most popular companion animal.

Cats

- 15.7 million cats in 2025

- Present in 1 out of 4 households

Down slightly from:

- 15.9 million in 2024

Dogs

- 10 million dogs in 2025

- Present in 1 out of 5 households

Compared with:

- 10.5 million in 2024

👉 Even with moderate declines, dogs and cats continue to dominate household pet ownership.

Smaller Pet Categories Show Mixed Performance

Some smaller categories recorded modest growth:

- Small animals:

- 4.4 million

- Up from 4.3 million

- Birds:

- Increased from 3.2 million to 3.3 million

- Fish:

- Increased from 2 million to 2.1 million

Meanwhile:

- Terrariums declined slightly to approximately 1 million

👉 The market is not collapsing —

but ownership growth is becoming increasingly limited.

Revenue Remains Stable Despite Softer Ownership Numbers

One of the most notable findings:

👉 Consumer spending remains resilient.

Germany’s pet market reached:

- €6.99 billion ($8.2B) in 2025

Compared with:

- €7 billion in both 2024 and 2023

- €6.5 billion in 2022

- €6 billion in 2021

👉 The market has largely stabilized at a high level.

Pet Food Continues to Drive the Market

Pet food remains the largest revenue contributor.

Pet Food Revenue

- €4.3 billion ($5B) in 2025

- Up 0.3% YoY

At the same time:

👉 Accessories experienced noticeable pressure.

Accessories Revenue

- Declined 4.6% YoY

- Reaching €1.1 billion ($1.2B)

This reflects a broader market pattern:

- Essential spending remains stable

- Discretionary purchases are becoming more cautious

Online Channels Continue to Expand

Retail channel performance shows ongoing structural change.

Total Sales

- Brick-and-mortar:

- €5.3 billion ($6.2B)

- Online:

- €1.5 billion ($1.8B)

The associations noted:

- Online sales increased 0.6% from 2025

- And are now 26% higher than in 2022

👉 Digital purchasing behavior continues to strengthen, even in a mature market like Germany.

Category Breakdown: Cats Lead Spending

Cat Food

Largest category overall:

- €2.3 billion ($2.7B)

Including:

- Wet food:

- €1.6 billion ($1.8B)

Dog Food

Generated:

- €1.7 billion ($1.99B)

With snacks leading growth:

- €768 million ($899M)

Other Pet Food Categories

Combined sales for:

- Bird food

- Fish food

- Small animal food

Reached:

- €204 million ($239M)

Accessories: Functional Categories Remain Important

Within accessories:

- Cat litter:

- €370 million ($433M)

- Cat accessories:

- €230 million ($269M)

- Dog accessories:

- €200 million ($234M)

Specialized pet retailers remained the dominant channel:

- 76% of accessories sales

👉 Functional and routine-use products continue to anchor spending behavior.

Final Insight

Germany’s pet market is no longer in a rapid expansion phase.

👉 It is transitioning into a mature, stability-driven market.

Key characteristics now include:

- Slower ownership growth

- Stable essential spending

- Greater caution in discretionary categories

- Rising importance of online retail

For brands, this means future competition will likely focus less on market expansion —

and more on:

👉 Value positioning

👉 Product differentiation

👉 Operational efficiency

Source: GlobalPETS