Household income and consumer spending remain key drivers of economic activity across major economies.

Between late 2025 and early 2026, several of the world’s largest markets showed positive momentum, with growth in retail, services, and overall consumption.

However, while demand appears to be expanding, geopolitical tensions — particularly those linked to ongoing conflicts in the Middle East — continue to introduce uncertainty.

👉 For businesses, this creates a mixed environment:

opportunity on the surface, but instability underneath.

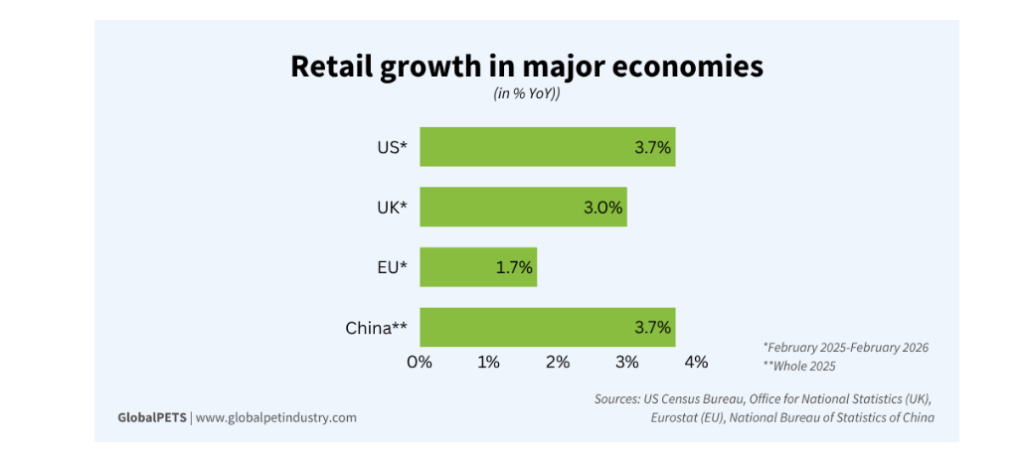

Retail Activity Shows Growth — Led by Non-Store Channels

Across major regions, retail performance remains positive, although growth rates vary.

United Kingdom

- Retail sales increased 0.7% over the three months to February 2026 (vs. the previous three-month period)

- Year-over-year growth reached 3%, marking the strongest quarter since February 2023

Growth was primarily driven by:

- Non-store retailers (mainly e-commerce), up 2.7%

- Peak activity recorded in January

Meanwhile:

- Food and household goods saw modest gains

- Department stores, textiles, and footwear declined

👉 This highlights a clear shift:

online and flexible retail formats are outperforming traditional segments.

United States

Retail and food service sales also showed solid growth:

- Up 3.7% YoY in February

- Total sales reached $738.4 billion (€630B)

Notably:

- Non-store retailers grew 7.5% YoY

- Miscellaneous retailers (including pet and pet supply stores) grew 11.6% YoY, the strongest category

👉 This is particularly relevant for the #petindustry:

category-specific growth is outperforming overall retail.

European Union

Growth remains steady but slower:

- Retail sales increased 1.7% YoY in both the EU and eurozone

Although sales declined slightly compared to the peak at the end of 2025:

- The long-term trend remains upward since 2021

By segment:

- Food, beverages, tobacco: +0.9%

- Non-food products: +2.3%

- Fuel (specialized stores): +1.6%

China

China recorded similar growth to the US:

- Retail sales increased 3.7% YoY

- Total retail sales reached ¥50.1 trillion ($7.3T / €6.3T) in 2025

Growth was driven by:

- Essential goods

- Upgraded consumption categories

👉 This reflects a dual pattern:

stable demand for basics alongside rising interest in higher-value products.

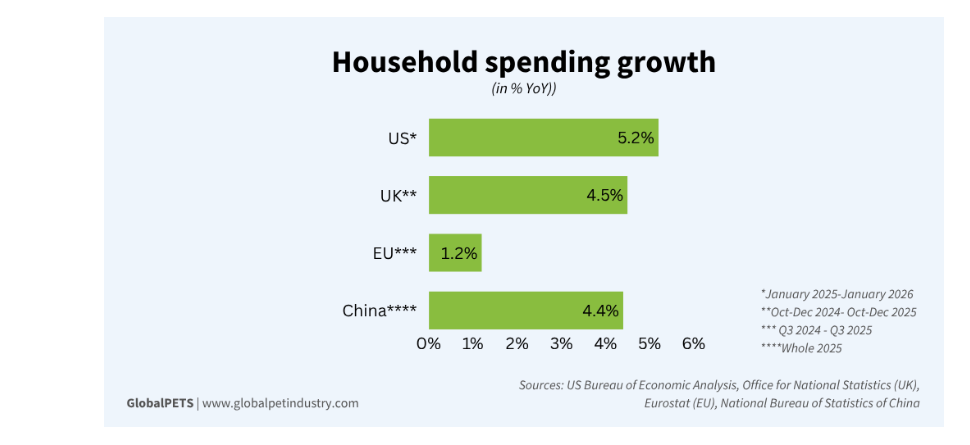

Household Spending Continues to Rise — But Structure Is Changing

United States

- Personal consumption expenditures rose 0.4% in January

- Personal income also increased 0.4%

- Total spending reached $21.5 trillion (€18.4T), up 5.2% YoY

Spending patterns show a shift:

- Stronger growth in services (healthcare, housing, utilities, financial services)

- Goods spending driven by:

- Food and beverages

- Recreational goods

- Vehicles

- Household equipment

👉 Consumers are prioritizing essential services while maintaining selective spending on goods.

United Kingdom

- Household spending grew 0.4% YoY (Q4 2025)

- Full-year growth reached 4.5% at current prices

- Seasonally adjusted growth dropped to 0.8%

Category insights:

- Recreational items, gardens, and pets: +2.1% (£51.2B)

- Pets and related products: -0.7% (£11.9B)

- Veterinary and #petservices: -2.7% (£6.5B)

👉 This reveals a key tension:

Spending is increasing overall, but pet-specific categories are facing selective pressure.

European Union

- Household consumption per capita increased 1.2% YoY (Q3 2025)

- Income per capita also rose 1.2% YoY

Both indicators have shown a steady upward trend since 2017 (excluding the pandemic period).

China

- Per capita consumption expenditure increased 4.4% YoY in 2025

- Faster growth in rural areas compared to urban regions

High-growth categories include:

- Miscellaneous goods and services: +11.2%

- Education, culture, recreation: +9.4%

- Transportation and communication: +8.3%

- Household facilities: +7.7%

Disposable income also increased:

- +5% YoY

Opportunities Exist — But Stability Is Not Guaranteed

Looking ahead, continued growth will depend on the balance between:

- Strong economic fundamentals

- External risks and disruptions

Positive factors include:

- Rising income levels

- Evolving consumption habits

- Growth in digital and service-driven spending

However:

👉 Ongoing geopolitical instability introduces the risk of sudden market disruption.

For companies, this means:

- Opportunities are real

- But so is volatility

👉 Agility is becoming essential — not just to capture demand, but to manage uncertainty.

Final Insight

The global retail environment is not slowing — but it is becoming more complex.

- Demand is growing

- But spending is becoming more selective

- Category performance is increasingly uneven

👉 For #petbrands, this means:

Understanding where growth is happening — and where pressure is building — is critical for making the right product and pricing decisions.

🔻 Part II Teaser

This is only part of the story.

In Part II, we’ll break down interest rates and inflation — and what they really mean for pricing pressure, margins, and demand in the #petmarket.

👉 If you’re navigating these shifts, it’s worth following.

Source: GlobalPETS

One Response